The most informative, educational, no-B.S. blog about Denver Market Trends and Denver Real Estate, by the Denver House Guy himself. Period.

Thursday, February 10, 2022

During Inflation, Savers Lose and Borrowers Win

Inflation, inflation, inflation. Why does it seem like everyone is talking about inflation? Well, for one thing, inflation is currently at a 40-year high. Yikes. And for another, inflation directly affects YOUR hard-earned money. It's important to try to understand how inflation does this, but with all the fear-mongering of the media, what may not be as discussed is how you can actuallybenefit from inflation.

The long and short of it is this: that during times of inflation, savers and lenders are losers, and debtors and investors are winners. Sound crazy? Read on.

What is inflation, and why does it matter to YOU?

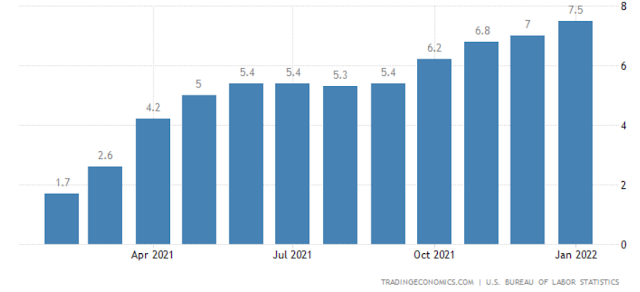

In simple terms, inflation is the decline of purchasing power of a given currency over time. The value of the dollar has been debased--we've printed too many dollars, and as the US Debt Clock shows, we are almost at $29,000,000,000,000 (trillion) in national debt, and counting. Another way to look at it is when the amount of spending and income grows faster than the production of goods, prices rise, this is inflation. Inflation is now at 6.2%, a 31-year high!

During inflation your money sitting in the bank goes down in value, right now at 7.5% per year (at least)! That means you must invest your money at a 7% annual return just to break even. If you don't, you are losing 7.5% per year! What does that mean? If you have $100,000 sitting in the bank, you are losing $7,000 per year, so next year your hard-earned money will be $92,500! And if you invest it and make 7.5% returns, it will only remain at the original $100,000. Crazy!

So how can real estate not only protect your money but maximize your profits during inflation? So glad you asked!

There are 3 ways that real estate can maximize your wealth during inflation.

1. This first concept blew my mind when I learned it. Just as your $100,000 sitting in the bank loses $7,500 per year, so does your real estate debt. If you borrow $100,000 from the bank today (instead of giving them your hard-earned $100,000 which represents thousands of hours of work!), your debt also loses the same inflation percentage per year, right now 7.5%! The best part is, the bank doesn't make you pay in inflationary-adjusted terms (tomorrow dollars), but only your original amount(yesterday's dollars). So next year I would only owe the bank $92,500, minus any payments I made. WOW. You can see how this hurts lenders, but very much helps debtors!

You make money in your sleep!

2. If you use that loan to buy real estate, real estate follows inflation, meaning if cost of goods and services go up, which they do during inflation, the cost of real estate prices also goes up. Your home or investment property will appreciate as well!

You make money in your sleep!

3. Just as real estate prices go up, historically rents go up as well. Rents have skyrocketed lately because of supply and demand issues, but historically rise during inflation as well.

You, once again, make money in your sleep!

And none of this includes the tax benefits of real estate!

So, when you buy cash-flowing real estate with long-term fixed interest rate debt, the Inflation Triple Crown that you win is: Price Inflation, Debt Debasement, and Cash Flow Enhancement(click for great video explanations).

Learning about these concepts epitomizes financial education.

You get to utilize a concept that impoverishes most people... and ethically turn it into your financial advantage.

TAKE AWAY HACK:

*Don't watch your money ERODE in your bank account! Invest it in cash-flowing real estate using debt which will be debased during inflation!